uae-taxconsultants.com

UAE Corporate Tax in 2026: Complete Compliance Guide for Mainland & Free Zone Businesses

An authoritative resource for business owners, finance leaders, and tax professionals seeking clarity and compliance in the evolving UAE tax landscape.

Gupta Group International

1/19/20265 min read

UAE Corporate Tax in 2026: Complete Compliance Guide for Mainland & Free Zone Businesses

The UAE’s corporate tax regime has swiftly become a cornerstone of the country’s economic and regulatory framework. What began as a transformative policy in 2023 has matured into a detailed compliance ecosystem. In 2026, corporate tax is not just about paying the correct amount — it’s about understanding exemptions, reliefs, thresholds, documentation requirements, and risks that can make or break your business’s legal standing.

Whether you run a mainland company or a free zone entity, mastering UAE corporate tax compliance is essential for risk management, business growth, and financial planning. This guide breaks down every key component — from registration and filing to advanced strategies that protect your tax position.

Chapter 1 — The Corporate Tax Landscape in the UAE (2026 Overview)

A Federal Tax With Local Impact-

The UAE’s Corporate Tax (CT) is a federal tax on business profits overseen by the Federal Tax Authority (FTA). It applies to most businesses operating in the UAE — including mainland companies, free zone entities, branches of foreign firms, and certain individual business operators.

Why Corporate Tax Relevance Has Grown in 2026-

The focus in 2026 has shifted from basic awareness to precision in compliance, relief application, and audit readiness. Errors in documentation, misapplication of exemptions, and misunderstanding Free Zone rules are now top triggers for fines and disruption.

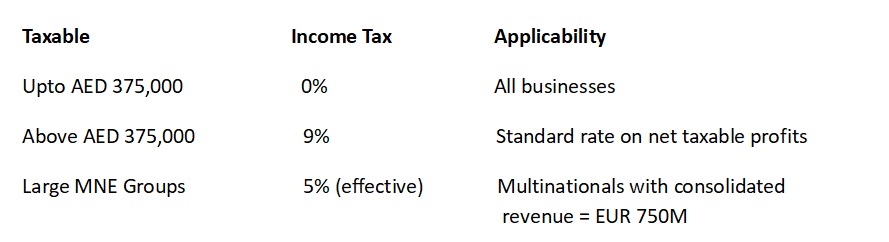

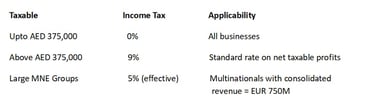

Chapter 2 — Corporate Tax Rates, Thresholds & Reliefs in 2026

* The Domestic Minimum Top-Up Tax (DMTT) increases the effective rate for large multinational enterprises under the OECD Pillar Two model starting January 1, 2026.

2) Small Business Relief:

To support SMEs, a special relief treats qualifying businesses with revenue ≤ AED 3 million as having zero taxable income for the relevant period. This option can provide significant relief — but comes with trade-offs such as limitations on tax loss carry-forward and interest deductions.

3) Free Zone Benefits and the Qualifying Free Zone Person (QFZP) Regime:

Unlike the misconception that “free zones are automatically 0% tax,” Free Zone benefits are conditional. To qualify for a 0% rate on qualifying income:

You must be a recognised Qualifying Free Zone Person (QFZP).

Your non-qualifying revenue must not exceed the lesser of AED 5 million or 5% of your total revenue.

Failing these conditions can trigger standard taxation at 9% on the entire taxable income for that tax year.

Understanding the tax rates and thresholds that determine liabilities is fundamental:

1) Standard Tax Rates:

Chapter 3 — Who Must Register & File Corporate Tax in 2026

Mandatory Registration:

Almost all businesses operating in the UAE must register for corporate tax with the FTA, regardless of whether they are profitable or not — including:

Mainland companies

Free Zone entities (even if they claim 0% rate)

Branches of foreign companies

Individuals operating professionally under certain conditions

Late registration can attract penalties — typically starting at AED 10,000 — even if no tax is due.

Which Entities Are Exempt or Special Cases:

Entities with profits under AED 375,000 are exempt from paying tax but must still register.

Some governmental and exempt entities may be excluded based on law.

Extractive industries often have separate emirate-level tax regimes and may fall outside the federal Corporate Tax net.

Free Zone entities can maintain 0% only by meeting strict qualifying conditions.

Chapter 4 — Corporate Tax Registration Process (Step-by-Step)

Step 1: Prepare Documentation

Collate these essentials before applying:

Valid Trade License

Financial statements (audited or reviewed)

Bank statements & general ledger

Contracts, leases, payroll, asset register

Details of ownership, capital structure, and legal representatives

Good record-keeping from day one is a major compliance advantage.

Step 2: Register via EmaraTax

All Corporate Tax registrations and filings must be done via the EmaraTax portal — the FTA’s electronic tax platform.

Log in using UAE Pass

Select “Corporate Tax Registration”

Complete business profile

Upload required documentation

Submit and monitor status

Step 3: Track Approval & TRN Assignment

Once approved, you’ll receive a Tax Registration Number (TRN). Use this in all future filings and correspondence.

Important Registration Tip

Even if your company expects zero profits or qualifies as a QFZP, register proactively — nil filings build a strong compliance record and avoid penalties.

Chapter 5 — Corporate Tax Filing & Payment Requirements

When to File:

Under the “9-Month Rule,” all taxable persons must:

File the Corporate Tax return within nine months from the end of the tax period.

Pay any Corporate Tax due by the same deadline.

Examples:

Fiscal year ending Dec 31, 2025 → Deadline: Sept 30, 2026

Year ending June 30, 2025 → Deadline: Mar 31, 2026

Nil Returns Are Mandatory:

Even if your business shows no profit or qualifies for exemption, a nil return must be filed. Failing to do so can attract fines and negatively affect license renewals.

Chapter 6 — Transfer Pricing & Documentation Compliance

Companies that transact with related parties must prepare transfer pricing disclosures and documentation:

Transfer Pricing disclosure forms with returns

Local file and Master file documentation available within 30 days of FTA request

Failing to maintain acceptable transfer pricing records is a leading cause of audit challenges.

Chapter 7 — Penalties, Risks & Non-Compliance Consequences

Penalties for corporate tax non-compliance in the UAE are strict:

Late registration: AED 10,000+

Late filing: AED 500–1,000 per month

Underpayment or incorrect return: Additional penalties and interest

Loss of Free Zone 0% status: Entire profit taxed at 9%, plus worse consequences

Proactive compliance prevents costly legal disputes, suspension of operations, or license renewal blocks.

Chapter 8 — Mainland vs Free Zone: Strategic Tax Differences

Mainland Businesses:

Standard 9% tax above AED 375,000

Full access to the UAE market without restrictions

Simpler substance requirements but no automatic 0% tax

Free Zone Businesses:

Free Zone entities have unparalleled potential to enjoy 0% tax — but only if they:

Meet QFZP criteria

Limit non-qualifying revenue within strict thresholds

Maintain adequate local substance and documentation

Falling short in any area can cause full taxable status and negate the Free Zone advantage.

Chapter 9 — Advanced Compliance: Audit Readiness & Best Practices

To ensure long-term compliance:

Maintain accurate books and financial records for at least 7 years.

Monitor related party transactions clearly.

Conduct quarterly internal reviews of your tax position.

Prepare for transfer pricing and documentation requests well in advance.

These practices vastly reduce audit risk and strengthen your tax position.

Chapter 10 — How Expert Tax Consulting Can Transform Your Compliance

Corporate tax compliance — particularly for free zones and international businesses — is complex and dynamic. Partnering with a professional UAE tax consultant can help you:

Navigate QFZP qualification and de minimis rules

Prepare flawless tax registrations and filings

Avoid common mistakes that trigger penalties

Strategize tax reliefs and planning

Build strong transfer pricing documentation

Ready to optimise your tax compliance in 2026?

Contact UAE Tax Consultants today for tailored support that protects your business and boosts financial confidence. Book a consultation now! (CTA)

Your Roadmap to Corporate Tax Compliance in 2026

In 2026, UAE corporate tax compliance is not just a statutory formality — it’s a strategic business function. Whether you operate on the mainland or within a free zone, understanding how tax law applies to your business can save you money, avoid penalties, and position you for sustainable growth.

Stay informed. Stay compliant. And when in doubt, lean on expert guidance to help you navigate complexities with confidence.

*Let UAE Tax Consultants be your trusted partner in compliance and growth — reach out today!

© 2026 uae-taxconsultants.com